Trump looks increasingly trapped over Iran as markets gyrate and oil shortage hits heartland

Donald Trump appears to be fast running out of exits on his Iran war folly.

Despite last night’s dramatic about face, and the huge reversals on Wall Street and commodity markets, the White House increasingly looks trapped.

Iran immediately refuted Trump’s claim that negotiations had even taken place, let alone that they were close to “a deal”.

The sudden shift from furious threats of impending doom to benign negotiator has been a hallmark of Trump’s leadership during his second term.

It has spawned a trading strategy so predictable and profitable that financial markets have coined the term TACO trade; Trump Always Chickens Out.

The routine goes something like this; threats of intimidation, leading to financial market upheaval before the inevitable backdown that sparks a huge relief rally.

On cue, Wall Street soared overnight and oil tumbled. But Iran’s Revolutionary Guard is fighting for survival, not financial gain, and appears determined to inflict maximum economic damage regardless of anything Trump says.

The messaging, even for this administration, has turned chaotic and wildly contradictory, causing markets and oil prices to perform a series of wild gyrations.

The only constant has been the president’s routine use of the word “obliterated”.

That’s apparently the fate of Iran’s military, air force and navy along with several layers of its leadership. And yet, the president last week was pleading for help from allies to open the Strait of Hormuz.

He then claimed that the US had achieved all its objectives, hinting that an end was in sight. But thousands of US marines are on their way to the now war-torn Persian Gulf.

Donald Trump’s meeting with Xi Jinping has been pushed back. (Reuters: Tingshu Wang)

Oil shortage hurts China

While it’s gone largely unnoticed, the White House over the weekend postponed a top-level meeting between Trump and his Chinese counterpart, Xi Jinping, that was due to start in about a week’s time.

There’s no definite date for a resumption, although White House officials have indicated it won’t be until the Iran conflict is wound up, or, in alternative reports, for about five or six weeks.

That may or may not give an indication of thinking within the administration as to how long it believes the bombardment will continue.

Early in the conflict, some analysts believed there was an ulterior motive behind America’s surprise attack on Iran — to build leverage over China.

Where Xi was dangling the threat of withdrawing critical mineral supply, the thinking was that Trump could counter with energy, particularly given America’s new-found status as the world’s biggest oil and gas producer and exporter.

Having recently kidnapped Venezuelan President Nicolás Maduro and shut off the supply of cheap, sanctioned oil to China, Trump was hoping to have control of Iran’s oil exports.

Almost 90 per cent of Iran’s oil exports are shipped to China. Again, it is cheap, sanctioned oil, often trading at $US15 a barrel below the market price.

While it makes up only slightly more than 13 per cent of China’s needs, the combined effect of both military operations has seen about 17 per cent of China’s oil needs suddenly out of the picture.

Meanwhile, Beijing’s other source of cheap oil, Russia, has suddenly had its sanctions status lifted, which elevates its oil export prices to global benchmarks.

That’s going to hurt.

China has been in the grip of a property market collapse that has undermined investment, impoverished households, sent inflation into reverse and forced authorities to downgrade growth to its lowest levels in decades.

Instead of holding the whip hand, Trump now finds himself a victim of his own making.

While China relies on almost half its imports passing through the Strait of Hormuz — which is now locked up — the US is also in the grip of gasoline shortages and soaring prices, just like everyone else.

The war has affected fuel supply in Australia. (AAP Image: James Ross)

Global oil and gas shortage to hit Trump heartland

The US might be a net exporter of oil, making it technically self-sufficient. But it still imports huge amounts.

Why? Because, as the old TV ad goes, “Oils ain’t oils.”

American oils are mostly light and low in sulphur and, given US refineries use a range of different crudes to produce the fuels they require, only about 60 per cent of the oil they use is produced at home.

The remainder comes mostly from Canada and Mexico with a small amount from the Persian Gulf, which makes America just as exposed to higher oil prices as everyone else.

National US gasoline prices have doubled in the past few weeks. Having demonised his predecessor Joe Biden for allowing fuel prices to get out of control, Trump is now facing the prospect of mid-term elections in the next few months amid soaring fuel prices.

That pressure alone may have been enough to prompt the president into his hugely embarrassing backflip. But it may well turn out to be ineffective.

The Strait of Hormuz is not international waters. It is controlled by Iran and Oman, although international shipping has the right to safely transit the narrow waterway.

The actual shipping lanes are just 3.2 kilometres wide, making global shipping, especially vessels loaded with fuel, easy targets for Iranian-made drones.

Even the mere threat of drone attacks is enough for insurers to run a mile, which is enough to keep the strait shut indefinitely.

Given the locally made drones cost as little as $US30,000 ($43,000), are brutally effective, easily concealed and simple to operate, they will be almost impossible to completely eradicate even if the large-scale assault continues.

Putin’s windfall, America’s soaring debt

Amid the chaos, the ongoing death and destruction, there’s at least one winner.

Vladimir Putin has been delivered a windfall. (Reuters: Sputnik/Vyacheslav Prokofyev)

Vladimir Putin, now embroiled in a grinding and brutal conflict in Ukraine for the past four years that is now costing his army 30,000 casualties a month, has finally been delivered a windfall gain.

Russian oil, banned in the West ever since the invasion and sold on the cheap to whichever nation was prepared to take the risk, is finally back on the open market.

America’s decision to lift sanctions on Russian oil has helped deliver an extra $US150 million a day from oil sales, adding billions of dollars to Putin’s war chest.

As a long-running ally of Iran, and a collaborator in its drone production, it will be in Russia’s interest to ensure the Strait of Hormuz is obstructed.

India and China, which have long purchased Russian oil despite the sanctions, are reported to have lifted buying orders.

US debt, meanwhile, has ballooned beyond $US39 trillion as the cost of financing the war adds to an already disturbingly large US deficit.

The yield on US 10-year bonds has risen alarmingly in the past three weeks, now sitting at more than 4.4 per cent, half a per cent higher than at the start of the war.

That only makes the debt burden worse and could dash any effort by the US Federal Reserve’s incoming chairman, Kevin Warsh, to cut interest rates.

Prepare for more turbulence.

Trump’s Economy Is Hurting Americans — and Setting Us Up for Long-Term Collapse

Trump boasts of a booming economy. He’s dead wrong. A year into Trump 2.0, the affordability crisis is worse than ever.

Truthout is an indispensable resource for activists, movement leaders and workers everywhere. Please make this work possible with a quick donation.

President Donald Trump is boasting about the economy one year into his term. He claims that inflation has been defeated, growth is unprecedented, incomes are rising, and his tariffs are generating hundreds of billions for the U.S. economy. This is all hogwash, according to progressive economist Gerald Epstein, a leading global authority on macroeconomic policy and finance.

In the exclusive interview for Truthout that follows, Epstein explains how, in reality, Trump’s policies have created an affordability crisis, and the growing deficit and humongous public debt are now bringing the country close to a tipping point.

C. J. Polychroniou: The state of the U.S. economy in Donald Trump’s first year of his second presidency has evolved in various ways. Trump, of course, has boasted on multiple occasions that the economy is “booming” and that the U.S. is the “hottest country anywhere in the world,” but there is plenty of data to suggest that the reality is quite different. There is apparently an affordability crisis and consumer confidencehas dropped to its lowest point in 12 years. Help us make sense of what’s going on with the economy under Trump 2.0. What exactly is the affordability crisis all about and how has it evolved since Trump’s return to the White House?

Gerald Epstein: Typical of Trump, he is boasting about the performance of the U.S. economy in the most hyperbolic terms. He even declared that his economy is “the greatest ever in history” in a recent interview on Fox Business Network. He points to the stock market and allegedly low inflation to back his claim. Is that the true state of the U.S. economy?

Donald Trump routinely barks that he inherited a terrible economy from Joe Biden and that he has turned it around: Now we have fast economic growth, low inflation, low consumer goods prices, high stock prices, and his great economy is going to get so good that it will be the best the world has ever seen. But basic economic data demonstrate that Trump’s boasts are simply wrong.

The best way to characterize the Trump economy compared to the economy the Biden administration left him, is this: Trump’s economy is mostly a continuation of Biden’s, but with a big tilt to the top, and with a big chance that it will soon run off the rails.

The overall inflation rate is about the same now (2.7 percent at the end of 2025) as it was when Biden left office (2.9 percent); the unemployment rate (4.3 percent in January 2026) is slightly higher than it was when Biden left office (4.1 percent). The rate of growth is similar, as well as the rate of growth of average real wages (wages minus inflation).

Some things are much worse, and these are directly connected to Trump administration policies and, ironically, run directly counter to Trump’s self-stated objectives. Trump’s tariffs have raised the cost of many U.S. goods, as well as the cost of food, and lowered the profits of medium-sized and small businesses, which, unlike big firms, have much less flexibility and fewer resources to adjust. Trump’s immigration dragnet has harmed economic activity in key sectors such as housing construction and services. Tax changes have greatly increased health care costs and pharmaceutical companies have raised prices on hundreds of medicines, all of which affect millions of people as these increased costs reduce their standards of living. And the trade deficit in goods has reached a new height.

Though first dissing “affordability” as a sham issue, Trump has now embraced it and tried to dominate it, claiming that he will get prices down across the board. But as numerous polls have shown, most people are not buying what Trump is selling. For example, a Wall Street Journal poll from September 2025 finds that the share of people who say they have a good chance of improving their standard of living fell to 25 percent, a record low in survey dating to 1987, and nearly 70 percent of people believe that the “American Dream” — if you work hard you will get ahead — is dead, the highest level in the 15-year history of the polls.

However, in addition to the direct damage Trump has done with tariffs, immigration outrages, and tax changes, we must look at the deeper, indirect and longer-term impacts of his policies.

Trump’s corporate giveaways and tax cuts, along with massive expenditures on the military and ICE [Immigration and Customs Enforcement], are creating unprecedented increases in the federal budget deficit and debt. This outcome could very well increase financial instability in the not-too-distant future. The increases in the national debt, unmatched by true investment in our economy, reduce our country’s net wealth.

In fact, the Trump administration has been a wealth destruction machine. This might seem surprising given the run up in the stock market, but that is small potatoes compared to the overall destruction across the board:

- “Department of Government Efficiency” (DOGE) destruction of basic research at universities and in the government, dismantling research projects and teams, some of which were producing breakthrough discoveries that could enhance future human well-being and productivity growth.

- DOGE firing of government workers with decades of experience — human wealth that will not easily be able to find similarly socially useful positions elsewhere.

- The tearing up of the rule of law, along with important infrastructure for wealth creation and sustainability.

- Secretary Robert F. Kennedy Jr.’s near destruction of the country’s health infrastructure, undermining the public’s health.

- The fossil fuel destruction of our climate.

So, has Trump solved our affordability problem? Far from it. If you think it is bad now, just you wait.

Studieshave found out that it is not foreign countries but U.S. consumers who are footing the bill for tariffs. If this is so, it would be logical to conclude that tariffs impact the purchasing power of low-income households, which in turn fuels the affordability crisis and may, subsequently, explain the sharp collapse in consumer confidence. Yet, there are those economistswho claim that the affordability crisis has nothing to do with tariffs. Can you shed some light on the connection between Trump’s tariffs and the affordability crisis?

At least one thing is clear: Trump’s tariffs are not helping with the affordability crisis. Importantly, this fact stands in contrast to what Trump, his tariff cheerleaders Peter Navarro and Commerce Secretary Howard Lutnick, among others, have claimed. They have repeatedly told us that the tariffs would generate free revenue financed by foreign countries that Trump and company could toss back to the American people like so much candy. This is false, since, as you point out, it is the American consumers (and to some extent businesses) who are paying the tariffs in the first place. They claimed that these tariffs would “bring back” high-paying manufacturing jobs — another boost to affordability for Americans. This, too, is false. Manufacturing employment has actually fallen by 83,000 jobs since Trump came into office. Finally, Trump claimed that tariff threats would force foreign governments and companies to lower prices on goods they sell to the United States. But there is no evidence that this is occurring.

One “bright spot” on the affordability spectrum has been the decline in gasoline prices. But this is not due to tariffs, but rather to the relentless obsession of the Trump administration with fossil fuels and, by ignoring climate change, his attempt to transform the entire human race into fossils themselves.

The U.S. dollar also appears to be collapsing under Trump. Why is that happening, and what risks does a weak dollar pose to the U.S. economy?

I think “collapsing” is way too strong, but it is true that the U.S. dollar is falling relative to the currencies of some crucial trading partners, including Europe. Over the past year, the dollar has fallen relative to the euro. And, oddly enough, this has occurred despite the fact that there has been a huge increase in foreign investments into the booming U.S. stock market. All else equal, more inflows of financial capital into the U.S. should have increased the value of the dollar. Why is the dollar getting weaker? It almost certainly has to do with the erratic international policies of the Trump administration, including the kidnapping of foreign leaders, the random bombing of fishing boats, the erratic missile attacks in disparate places around the world from Nigeria to Iran, and the threats of invasion of our former allies — from Denmark to Canada. This is all joined by roving bands of out-of-control paramilitary forces on the streets of major American cities.

The U.S. dollar used to be a “safe haven” in the global financial world. When the world got tough, the tough bought the dollar. Now they ditch the dollar and buy gold and silver, whose prices have been mostly skyrocketing of late.

What risks does the apparent fraying of the dollar’s safe haven role and international role more generally have for the people of the United States? This question invites intense disagreement among economists who argue under the rubric of whether the U.S. dollar has created an “exorbitant privilege” for the United States.

When the world eagerly wants to hold dollars, it is easier for the United States to borrow from the rest of the world at a relatively cheap rate. This allows the U.S. government to shower favors on some Americans by cutting their taxes and to build bombs and aircraft carriers for others, all on money borrowed cheaply from foreigners: an exorbitant privilege indeed. Other economists claim this privilege is relatively small and we shouldn’t make too big a deal about it.

The issue is highly relevant. The United States government has been borrowing billions of dollars for decades now. The Congressional Budget Office recently told us that, with the reckless spending and tax giveaway policies of the Trump administration, the annual federal deficit will grow from $1.9 trillion in 2026 to $3.1 trillion in 2036, and the federal debt held by the public will rise from 101 percent of GDP this year to 120 percent in 2036, surpassing its previous high of 106 percent in 1946, just after World War II.

If foreigners lose more confidence in the dollar and U.S. treasury debt, the interest rates we have to pay on all this debt will go up and, if the rate gets higher than the growth rate of our economy, our debt payments relative to the size of our economy could grow, and grow and grow.

Is the U.S. likely to suffer a Venezuela-style collapse? Probably not. But as foreign investors and speculators get nervous, a shock like an international crisis, or big spike in oil prices, could be a weighty straw on a fragile camel.

Is a weak dollar good or bad for low-income households?

Generally, a weak dollar has two effects. It makes imports more expensive, so in that sense, acts like a tariff: not good for low-income households. On the other hand, it can make our exports more competitive and expand these exports. Will this benefit low-income households? Only, for the most part, if they work in export industries and they have the bargaining power to insist on getting some of the spoils accruing to the bosses from their improved export position. Usually, workers in low-income households do not have such bargaining power, as the neoliberal project of the last 35 years or so has decimated private unions.

Is the dollar doomed?

No. The most likely outcome is that it will continue to lose some of its luster, and like the rest of the U.S. economy under the Trump orgies of slash-and-burn economic policy, it will become just one among many internationally used currencies, rather than the coin of the global realm.

Trump’s changing course on Strait of Hormuz strategy raises questions about US war preparation

WEST PALM BEACH, Fla. (AP) — At war with Iran, President Donald Trump is cycling through an increasingly desperate list of options as he searches for a solution to the crisis in the Strait of Hormuz. He has jumped from calls to secure the waterway through diplomatic means to lifting sanctions and now escalating to a direct threat against civilian infrastructure in the Islamic Republic.

Trump and his allies insist they were always prepared for Iran to block the strait, yet the Republican president’s erratic strategy has fueled criticism that he is grasping for answers after going to war without a clear exit plan. On Saturday came his latest attempt, via an ultimatum to Iran: Open the strait within 48 hours or the United States will “obliterate” the country’s power plants.

Trump’s aides defended the threat as a hard-edged tactic to press Iran into submission. Opponents framed it as the failure of a president who miscalculated what it would take to get out of a geopolitical mire.

“Trump has no plan to reopen the Strait of Hormuz, so he is threatening to attack Iran’s civil power plants,” said Sen. Ed Markey, D-Mass, adding: “This would be a war crime.”

“He’s lost control of the war and he is panicking,” said Sen. Chris Murphy, D-Conn., responding to Trump’s post.

Over the course of about a week, Trump has repeatedly shifted his approach on the crucial waterway for global oil and gas transport. There is growing urgency for Trump as soaring oil prices rattle global markets and pinch American consumers months before pivotal midterm elections.

Trump and diplomacy

Trump tried his hand at a diplomatic solution last weekend when he called for a new international coalition to send warships to the strait.

Allies turned him down. Trump then said the U.S. could manage on its own. On Friday he suggested other countries would have to take over as the U.S. eyes an exit. Hours later he indicated the waterway would somehow “open itself.”

“You can’t all of a sudden walk away after you’ve kind of created the event and expect other people to pick it up,” Sen. Thom Tillis, R-N.C. told ABC’s “This Week.”

Trump’s Treasury Department on Friday made its latest attempt to get a handle on soaring gas prices, by lifting sanctions on some Iranian oil for the first time in decades. That relieved some of the pressure that Washington traditionally has used as leverage against Tehran.

The goal was to send millions more barrels of oil into the global market. It is not clear, however, how much of a dent that would make in lowering pump prices or how the administration could prevent Iran from cashing in on the renewed sales.

The administration earlier temporarily lifted sanctions on some Russian oil.

An ultimatum to Iran

Trump’s ultimatum, conveyed while he spent the weekend in Florida, carries a threat of remarkable aggression. His previous messaging mostly focused on U.S. success in hitting Iran’s air force, navy and missile production. This time, the threatened target is the energy infrastructure that powers hospitals, homes and more.

His social media post — 51 words, much of it in capital letters — did not have the appearance of a message that underwent the careful legal scrutiny needed to justify an attack on civilian infrastructure, said Geoffrey Corn, a law professor at Texas Tech University and a retired lieutenant colonel in the Army who served as a military lawyer.

“It certainly has a feeling of ready, fire, aim,” Corn said of Trump’s moving strategy.

“He overestimated his ability to control the events once he unleashed this torrent of violence.”

That type of widespread attack would probably be a war crime, Corn said. For military leaders, it could force a choice between obeying an order to carry out a war crime or refusing and facing criminal sanction for willful disobedience, he said.

Laws governing warfare do not explicitly forbid attacks on power plants, but the tactic is allowed only if an analysis finds that the military advantages outweigh the civilian harm, legal scholars say. It is seen as a high bar to clear because the rules of war are, at their core, designed to separate civilian and military targets.

Iran’s U.N. ambassador, in a letter to the Security Council, warned that the deliberate targeting of power plants would be inherently indiscriminate and a war crime, according to the state-run IRNA news agency.

The White House has already faced intense backlash after the U.S. was blamed for a missile strike on an Iranian elementary school that killed more than 165 people.

Trump aides justify latest attempt to rein in the crisis

Trump provided scant detail on which plants might be targeted and how. He gave Iran until Monday to reopen the strait or else the U.S. will strike “various POWER PLANTS, STARTING WITH THE BIGGEST ONE FIRST!”

Trump’s team came to his defense Sunday, offering justification for striking Iran’s energy grid.

Mike Waltz, the U.S. ambassador to the United Nations, said Iran’s Revolutionary Guard controls much of the country’s infrastructure and is using it to power the war effort. He said potential targets include “gas-fired thermal power plants and other types of plants.”

Speaking on Fox News, Waltz said he wanted to get ahead of “hand-wringing” from the global community, calling the Revolutionary Guard a terrorist organization. “The president is not messing around,” he said.

NATO’s secretary-general, Mark Rutte, who has allied himself closely to Trump, tried to calm tensions. He said he understood Trump’s anger and stressed that more than 20 countries are “coming together to implement his vision” of making the strait navigable as soon as possible.

Israel’s ambassador to Washington, Yechiel Leiter, cautioned against an all-out attack like the one Trump threatened. “We want to leave everything in the country intact, so that the people who come after this regime are going to be able to rebuild and reconstitute,” he told CNN’s ”State of the Union.”

Trump’s threat could prove counterproductive: If it’s carried out, Iranian leaders said they would completely close the strait and retaliate against U.S. and Israeli infrastructure.

Three Nations Mediate Talks Between U.S. and Iran

U.S. President Donald Trump stated that indirect contacts with Iran have made progress, but Tehran denies that negotiations with Washington are taking place…

U.S. President Donald Trump said on Monday (March 23) that the U.S. and Iran have reached “some major points of agreement” during contacts—reportedly taking place through the mediating roles of Turkey, Egypt, and Pakistan.

According to the news site Axios, on Sunday, the three mediating countries passed messages back and forth between Washington and Tehran. A source cited by Axios stated that both sides were ready to resume dialogue at that time. This source said the Iranian side showed goodwill, while the U.S. side also wanted to push for exchanges amid sharp fluctuations in financial markets and oil prices.

The Axios source stated that the Foreign Ministers of Egypt, Pakistan, and Turkey held separate discussions with U.S. Middle East Envoy Steve Witkoff and Iranian Foreign Minister Abbas Araghchi.

According to Axios, Egyptian Foreign Minister Badr Abdelatty held phone calls on Sunday with Mr. Witkoff, Mr. Araghchi, and counterparts from Pakistan, Turkey, and Qatar. During these exchanges, Mr. Abdelatty emphasized the need to restrain the spillover effects of the conflict and prevent the situation from further escalating.

“Mediation efforts are still being promoted and have made progress. Discussions are currently focused on ending the war and handling outstanding issues. We hope to have an answer soon,” the aforementioned source said.

Speaking to reporters in Florida before boarding Air Force One on March 23, Mr. Trump said the exchanges—which according to him took place with a “very respected” Iranian official—focused on ensuring Iran abandons its nuclear ambitions and its stockpile of enriched uranium.

“The U.S. has eliminated the first-tier, second-tier, and most of the third-tier leadership of Iran,” Mr. Trump said, stating that Washington is currently still working with the person he considers the most respected figure and the one holding the leadership role.

Mr. Trump emphasized that the U.S. does not accept Iran continuing to enrich uranium, and simultaneously wants to take control of the previously enriched uranium volume. He also stated that Envoy Witkoff and his son-in-law, Mr. Jared Kushner, participated in the discussions. According to Mr. Trump, contacts began on Sunday, continued into Monday, and could soon lead to an agreement if progress goes favorably.

Earlier, on the social network Truth Social, Mr. Trump stated that the U.S. and Iran had “very positive and constructive exchanges” over the past two days, aimed toward a comprehensive solution to end the conflict in the Middle East. He made this statement when explaining the decision to postpone U.S. strikes on Iran’s energy infrastructure for five days.

However, on Monday, Iranian Parliament Speaker Mohammad Bagher Ghalibaf rejected reports that Tehran had negotiated with Washington, while asserting there were “not any negotiations” between the two sides.

On the social network X, Mr. Ghalibaf suggested that such information is “fake news,” released to influence financial markets and oil prices, while helping the U.S. and Israel find a way out of the current stalemate.

Mr. Trump’s announcement regarding the postponement of the plan to attack Iran’s energy infrastructure pushed stock prices up, while oil prices dropped sharply to below $100 per barrel. This development completely reversed the previous sell-off wave on the stock market following Mr. Trump’s threats over the weekend and the retaliatory declaration from the Iranian side.

Meanwhile, the Reuters news agency cited a European official as a source stating that although the two countries have not had direct negotiations, Egypt, Pakistan, and Gulf countries are still passing messages back and forth between the two sides. A Pakistani official stated that U.S. Vice President JD Vance, along with Mr. Witkoff and Mr. Kushner, are expected to meet Iranian officials in Islamabad this week.

![]()

What is the impact of Trump 2.0 on the global economy?

A look at how President-elect Donald Trump’s return to power could reshape the global economy with higher US growth, inflation, and significant policy shifts.

Nonetheless, our working assumptions of an impending Trump 2.0 and its effect include:

- A sharp increase in the average tariff on China from 15% to 40% starting early in 2025, isolated spats with other trade partners, but the avoidance of a global baseline tariff.

- Extension of the Tax Cuts and Jobs Act in late 2025, with some additional measures, including reducing corporation tax from 21% to 20% (15% for some companies), higher defense spending, and modest spending cuts elsewhere so that fiscal policy is loosening by 0.5% of GDP in 2026.1

- A significant rise in deportations to 750,000 a year, which, alongside border restrictions and deterrence, means net migration falls from 3 million per annum to essentially flat.

- Deregulation, including a relaxation of anti-trust measures and more lenient bank capital requirements.

Potential growth boost

We expect US gross domestic product (GDP) growth to remain robust next year at 2%, reflecting a cooling, but still solid, labor market and strong corporate profitability.

We’ve upgraded our 2026 forecast by 0.2% to 2.2% because we expect fiscal loosening and deregulation to more than offset tariffs. However, this boost is likely to fade as the immigration changes take effect, and the level of real GDP could be lower than it would have been by the end of Trump’s term.

Higher tariffs, strong demand, and lower labor supply mean we’ve increased US inflation forecasts. We see core personal consumption expenditures (PCE) inflation at around 0.2% and 0.4% higher in 2025 and 2026, respectively, leaving it stuck at around 2.5%.

We therefore expect the Federal Reserve (Fed) to deliver fewer rate cuts. We forecast just three in 2025, with the Fed funds rate target range settling at 3.50%–3.75%. Additional rate reductions in 2027 and 2028 are possible as the economy eventually slows.

US

Activity

US growth is being supported by a resilient consumer, a labor market that, while cooling, remains solid, and strong corporate profitability. Trump’s second term will see tax cuts, higher defense spending, and looser regulatory policy, which should further boost growth as the policies take effect mostly in 2026. However, these tailwinds will be dampened by rising tariffs and slower net migration, which constitute negative supply shocks. Indeed, we think these will weigh on growth in 2027 and 2028. There is a risk the policy mix is more disruptive, with broader tariffs and large-scale deportations, or of a growth-friendly mix that focuses less on these policies and more on deregulation.

Inflation

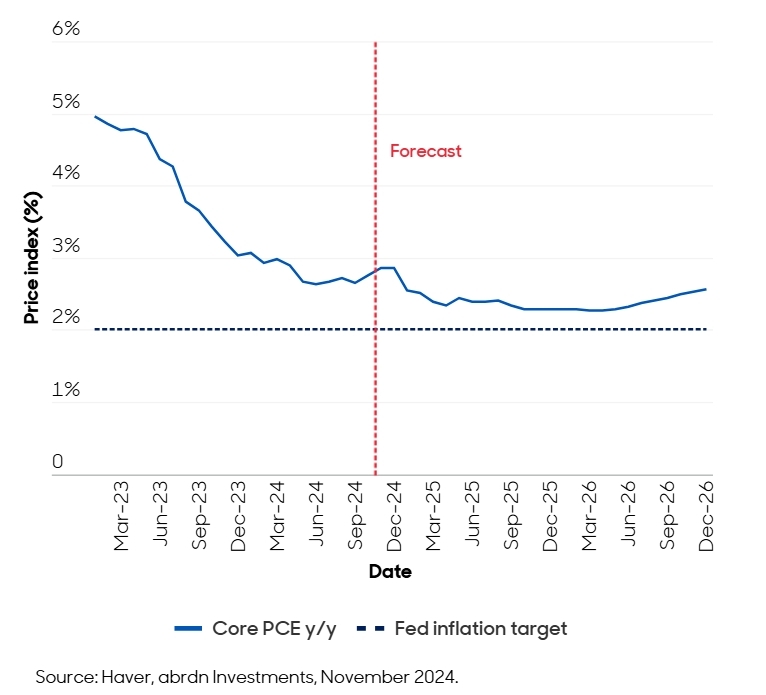

We believe the combination of demand-side stimulus, in the form of looser fiscal policy, and shocks to the supply side, via tariff hikes and deportations, will leave inflation stuck near 2.5% (Chart 1).

Chart 1. US core PCE set to remain stubbornly above target in the face of an inflationary policy agenda

Moreover, risks of a reacceleration have increased, especially in the case of large rises in tariffs or aggressive deportations. Indeed, the pandemic illustrates how swings in aggregate demand and supply can trigger rapid price adjustments. So, only a more toned-down version of Trump’s policy agenda would leave the current trend of disinflation toward the target intact.

Policy

The Fed looks set to cut in December, even if recent firm inflation data have cast some doubt over this move. Assuming no nasty surprises in November CPI, a 25 bps-move would reduce rates to 100 bps over the past three meetings. This adjustment will slow in 2025, when we expect the Fed to cut by just 75 bps, reflecting a careful approach as rates get closer to equilibrium levels and inflation progress is interrupted by Trump’s policy agenda.

After that, we believe rates will remain on hold at 3.50–3.75% through 2026, before cuts resume as growth and inflation slow.

China tariffs and stimulus

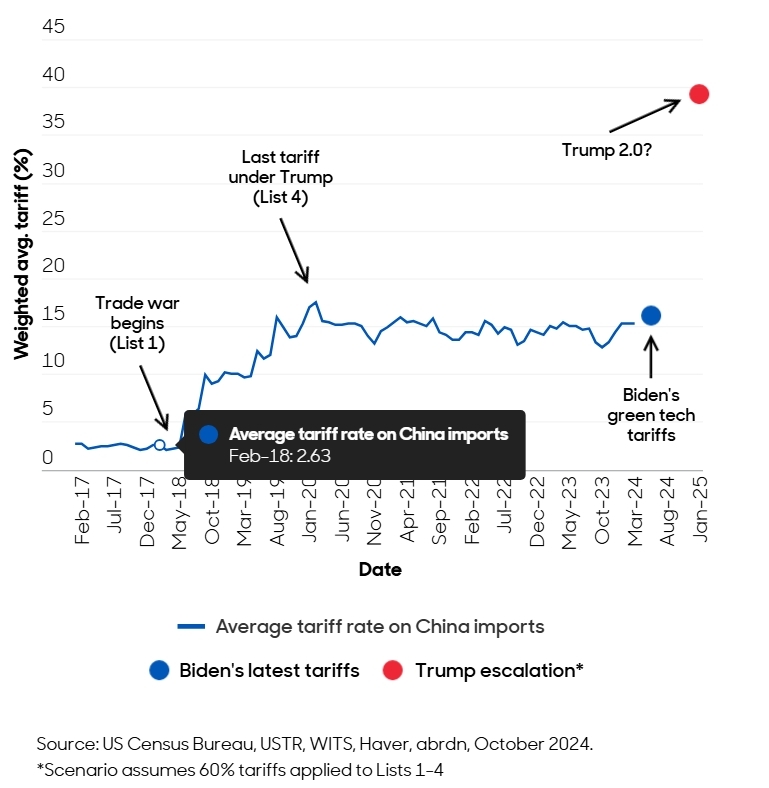

In China, we see tentative green shoots in the data, so we forecast GDP growth of 4.8% in 2024. However, we have made meaningful downgrades to our 2025 (to 4.3%) and 2026 (to 4.1%) numbers – totaling 1% off the GDP level. This would be around double the estimated impact from the first trade war (during Trump’s first term), reflecting the sharper increase in tariffs (Chart 2).

Chart 2. Tariffs facing Chinese exports are likely to more than double as a second trade war unfolds

Chinese tariff retaliation is almost inevitable, although we do not expect it to match the size of US measures, given China’s cyclical weakness. Instead, we anticipate targeted measures such as agricultural tariffs, critical mineral export restrictions, and action against US companies in China.

Policy stimulus is likely to continue as the trade war intensifies, but it could continue to fall short of market expectations. Large-scale consumption support does not align with policymakers’ reading of the economy or their de-risking agenda. Currency depreciation may not match US tariff increases because of financial stability risks.

China is, therefore, a source of important risks to our forecasts.

Emerging markets’ potential winners and losers

Heightened trade uncertainty and a more inflationary backdrop in the US will be difficult for emerging markets (EMs) to navigate. EMs with large trade surpluses (Mexico, Vietnam, Korea, and Taiwan), those re-exporting Chinese goods (Vietnam, Malaysia, Mexico), or countries with high tariffs on their imports of US goods (Brazil, India) are likely to face at least periodic market pressure.

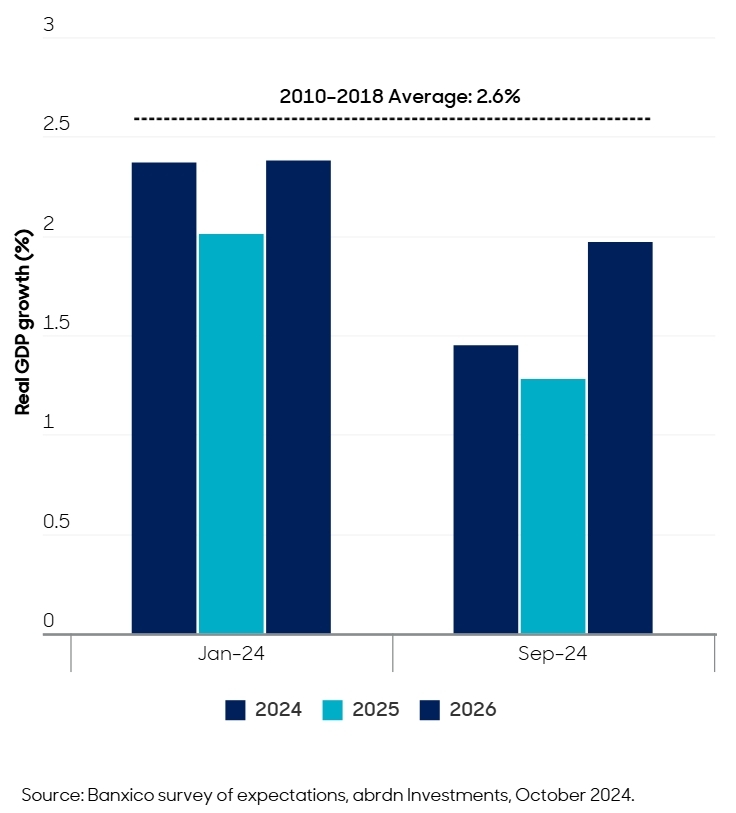

Mexico’s deep economic links with the US make it vulnerable (Chart 3). Still, we believe threatening a renegotiation of the United States-Mexico-Canada Agreement is a way of pressuring Mexico to stem migration into the US. Ultimately, as the US distances itself from China, it will need to rely more on other countries, like Mexico and India, which are poised to gain from reshoring.

Chart 3. Domestic demand in Mexico and cross-border uncertainty have dampened growth forecasts

Trump’s reflationary policy agenda will pressure the Fed-sensitive EM central banks (Mexico, Indonesia) and those for which concern about fiscal policy is highest (Brazil). But the second-round effects of trade actions on China may trouble more countries in the long run. Weaker Eurozone growth and the risk of more competition from China may hurt Eastern Europe.

Europe, UK, and Japan

Heightened trade uncertainty means we have lowered our Eurozone GDP forecasts by 0.2%–0.3% for 2025 and 2026. We’ve also increased our inflation forecasts by about 0.1% each year. We think the European Central Bank will pursue a slightly more aggressive easing path than previously expected, lowering the policy rate to 2% by the second half of 2025.

Beneath these relatively limited aggregate effects, there is divergence. In particular, the German auto industry could suffer from trade measures, while broader headwinds from global industrial weakness and unnecessarily tight fiscal policy will remain in place.

The UK’s exports are dominated by services and less likely to see tariffs. In fact, we’ve increased our growth forecast for 2025 after the recent budget delivered easier fiscal policy support. But higher gilt yields have removed the government’s fiscal headroom, making further tax increases possible.

Finally, the Bank of Japan (BoJ) should continue slowly increasing interest rates. We expect the next hike in January. With US rates higher, the BoJ will now bear more of the burden of supporting the yen by closing the US-Japan rate differential, which may encourage more rapid hiking.

Final thoughts

With the coming of Trump’s second administration, we expect higher US growth, inflation, and fewer Fed rate cuts. Material deregulation and reform of the tax code could help boost potential growth and push up equilibrium rates in the long run. For the rest of the world, we have revised our forecasts with growth (down) and inflation (up) in anticipation of more monetary policy divergence. Finally, we believe the Trump effect will likely be less disruptive than many investors may fear.

1 The Tax Cuts and Jobs Act was signed into law on January 1, 2018. This law brought sweeping changes to the tax code and impacted individuals depending on their income level, filing status, and deductions.

Important information

Projections are offered as opinion and are not reflective of potential performance. Projections are not guaranteed and actual events or results may differ materially.

Foreign securities are more volatile, harder to price and less liquid than U.S. securities. They are subject to different accounting and regulatory standards, and political and economic risks. These risks are enhanced in emerging markets countries.

:max_bytes(150000):strip_icc():focal(753x271:755x273):format(webp)/cole-the-deaf-dog-112125-1a-ad248101bd174108a795d88d6afd93d8.jpg?resize=750,500&ssl=1 "Elementary School Throws Deaf Therapy Dog a Surprise Birthday Party as Students Learn Sign Language to Sing ‘Happy Birthday’")

:max_bytes(150000):strip_icc():focal(749x0:751x2):format(webp)/Amanda-Burritt-Emma-1-110525-fd409072cc9e43a58476b5e0079872fd.jpg?resize=750,500&ssl=1 "Mom Captures the Shocking Moment She First Realized Her Baby Daughter Went Blind (Exclusive)")

:max_bytes(150000):strip_icc()/GettyImages-2285630301-a122cc16a1234420b9a3488af7ca36ec.jpg?resize=1500,1032&ssl=1 "Harry and Meghan still want U.K. return as they feel ‘unwelcome,’ ‘outcast’ in U.S.")

:max_bytes(150000):strip_icc():focal(749x0:751x2)/rodham-3-4ded923ef9d94f978df175d5a2241bf4.jpg?resize=1500,1000&ssl=1 "The Heartbreaking Farewell: Bill Clinton’s Most Emotional Public Address Shakes the Nation to Its Core")

:max_bytes(150000):strip_icc():focal(967x412:969x414)/Anne-Hathaway-Odyssey-premiere-2026-071626-e4f5e979023c4dfda5a6153163f6f515.jpg?resize=1500,1000&ssl=1 "Anne Hathaway ‘In Shock’ Over Pregnancy at 43")

:max_bytes(150000):strip_icc():focal(731x264:733x266)/kim-kardashian-101525-4-63bb00fd35ad4b6fa3867d6df11203c2.jpg?resize=1500,1000&ssl=1 "Kim’s revenge – my wedding will top Taylor’s")